04/08/2023

Eleven years of governorship of Jorgovanka Tabaković – stability, security and innovations as the common interest of all market participants

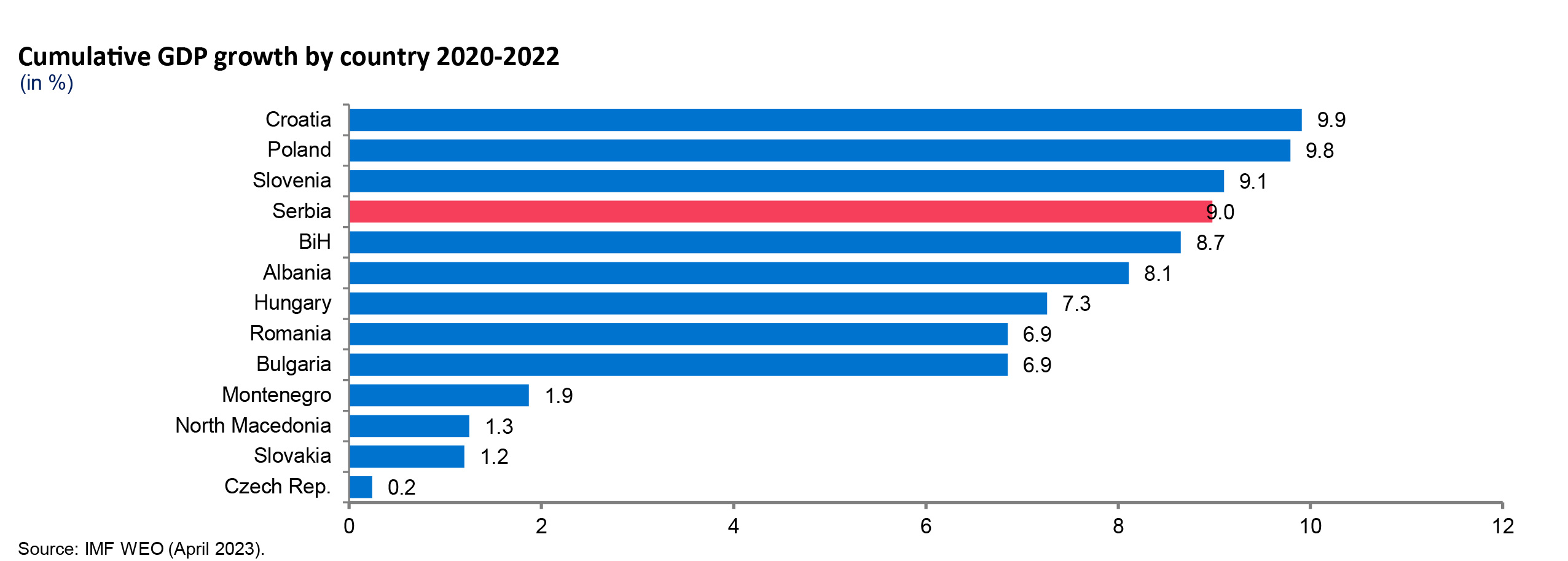

During the last eleven years, Serbia traversed the path from being a country of monetary and financial instability and uncertainty to becoming a country with inflation levels comparable to other countries, a stable currency, record level of FX reserves, stable financial system, sound public finance, solid investment growth, strong export growth and a sustainable external position.

“One’s entire life is about giving an account. And telling a story of what we have done. The results always paint the most vivid picture. But they don’t speak about themselves if we are silent. Stability has become the new reality for Serbia. Nobody looks at exchange rate lists with trepidation anymore. Confidence that is indispensable and committing, is deserved only if the results are felt by the citizens and corporates. There are no strategies and tactics about that. To think and respond timely, or before the crisis breaks out, and to be decisive in the implementation of measures, at the cost of initial misunderstanding and resentment by certain interest groups – all of this was necessary for NBS success. To me, stability has always been the point where the interests of all meet – the interests of creditors and debtors, investors and depositors, government and citizens, importers and exporters. This is the point of equality where there are no favourites. Hence, I offer an insight into the results that testify to the possibility to fix the system which proves its purpose only if we work to the benefit of all”, states Governer Jorgovanka Tabaković.

RESULTS:

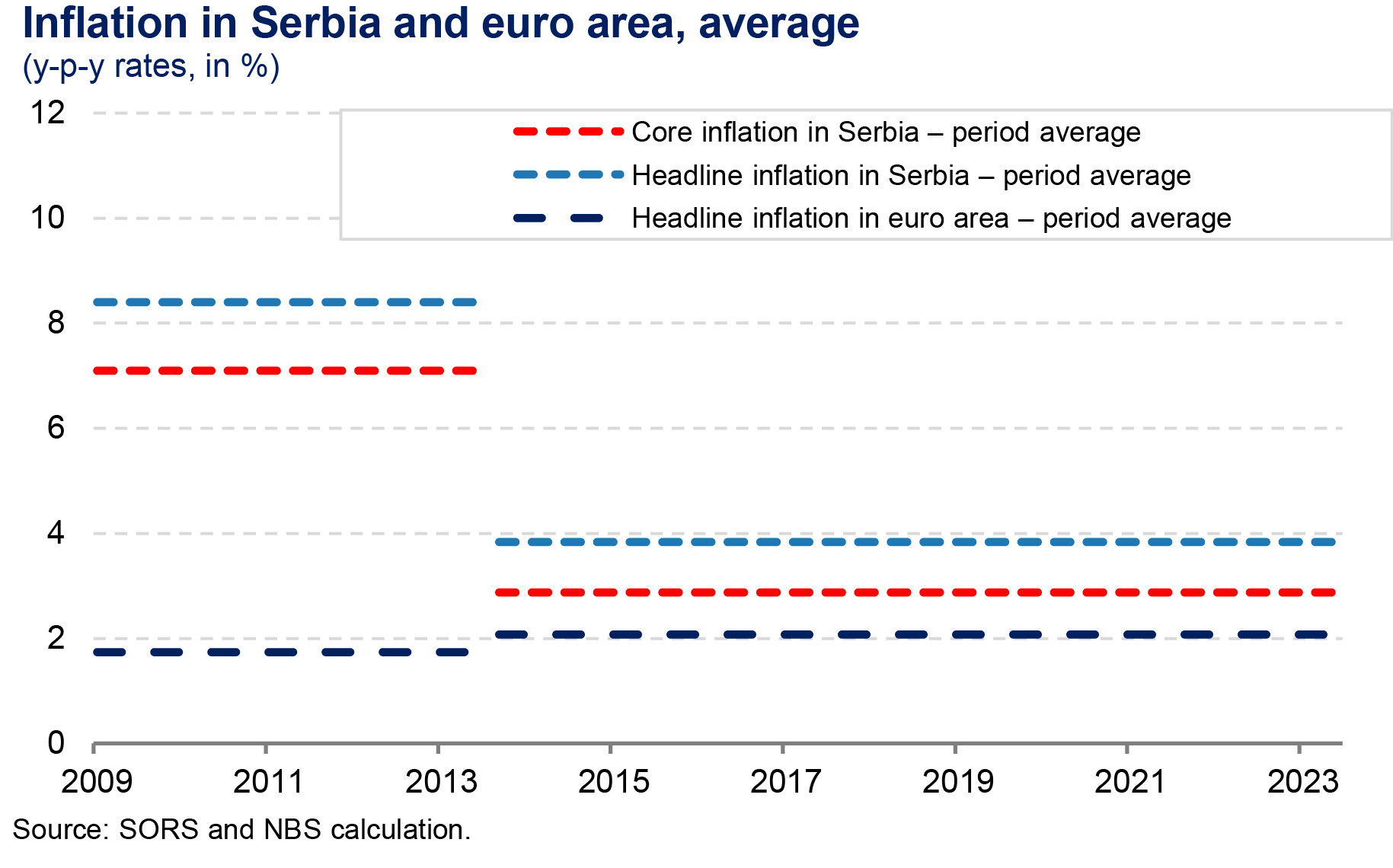

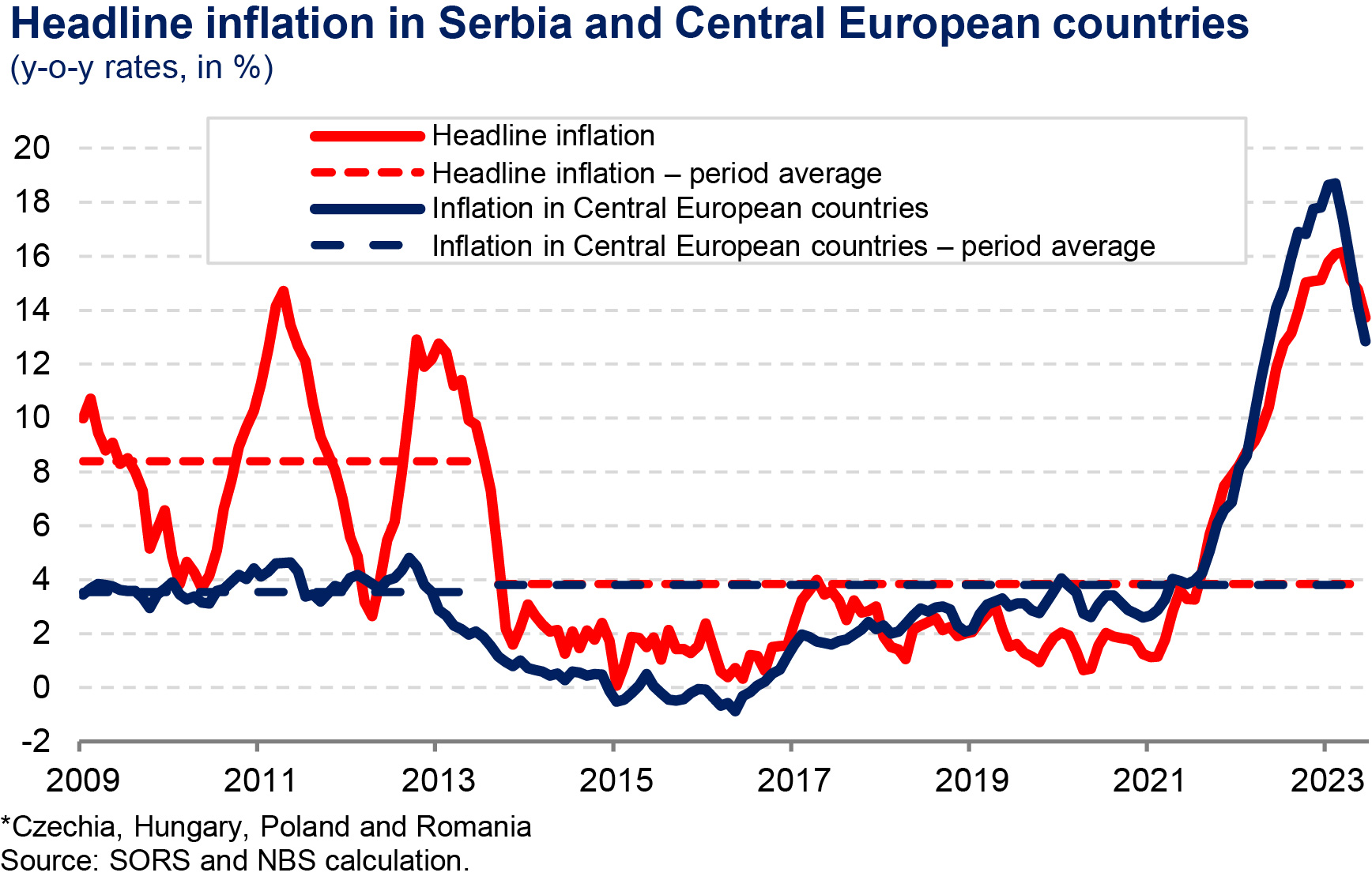

- With adequate monetary policy we reduced inflation by 10 pp in a year – from 12.2% at end-2012 to 2.2% at end-2013. Pressures abated as a result of restrictive monetary policy measures taken in the period June 2012 – February 2013, a drop in the prices of primary agricultural commodities (in the domestic and global market), low domestic demand and anchoring of inflation expectations. The total effect was amplified by curbing excessive short-term volatility of the dinar exchange rate and establishing full coordination with fiscal policy. After reducing inflation, we maintained it continuously low until global inflationary pressures escalated.

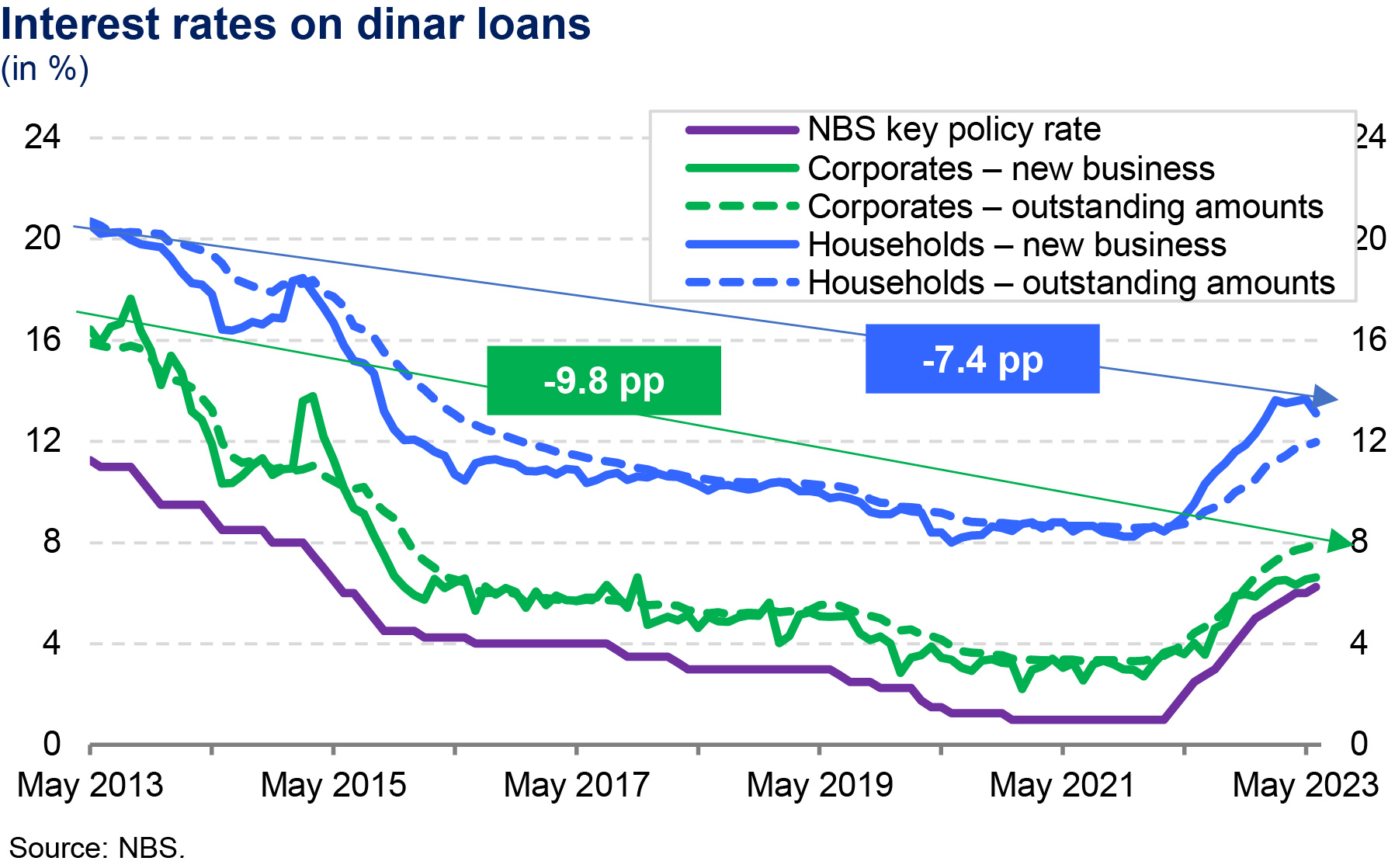

- Having suppressed inflationary pressures, we initiated the cycle of monetary policy relaxation in May 2013. The key policy rate was lowered from 11.75% to 9.5% at end-2013. We proceeded with the rate cuts in the following years, bringing the rate down to 1% at end-2020, where it was kept until April 2022.

- Owing to Serbia’s better macroeconomic position and more favourable outlook, in November 2016, in cooperation with the government of the Republic of Serbia, we adopted the decision on lowering the inflation target from 4% to 3% as of 2017, with unchanged tolerance band of ±1.5 pp. By setting the target at a lower level, we showed our determination to preserve low and stable inflation over the medium run, together with the government of the Republic of Serbia. This further contributed to the anchoring of long-term inflation expectations of the financial and corporate sector, to the predictability of the business and investment environment, a decline in long-term dinar interest rates, and a greater use of the dinar in financial transactions.

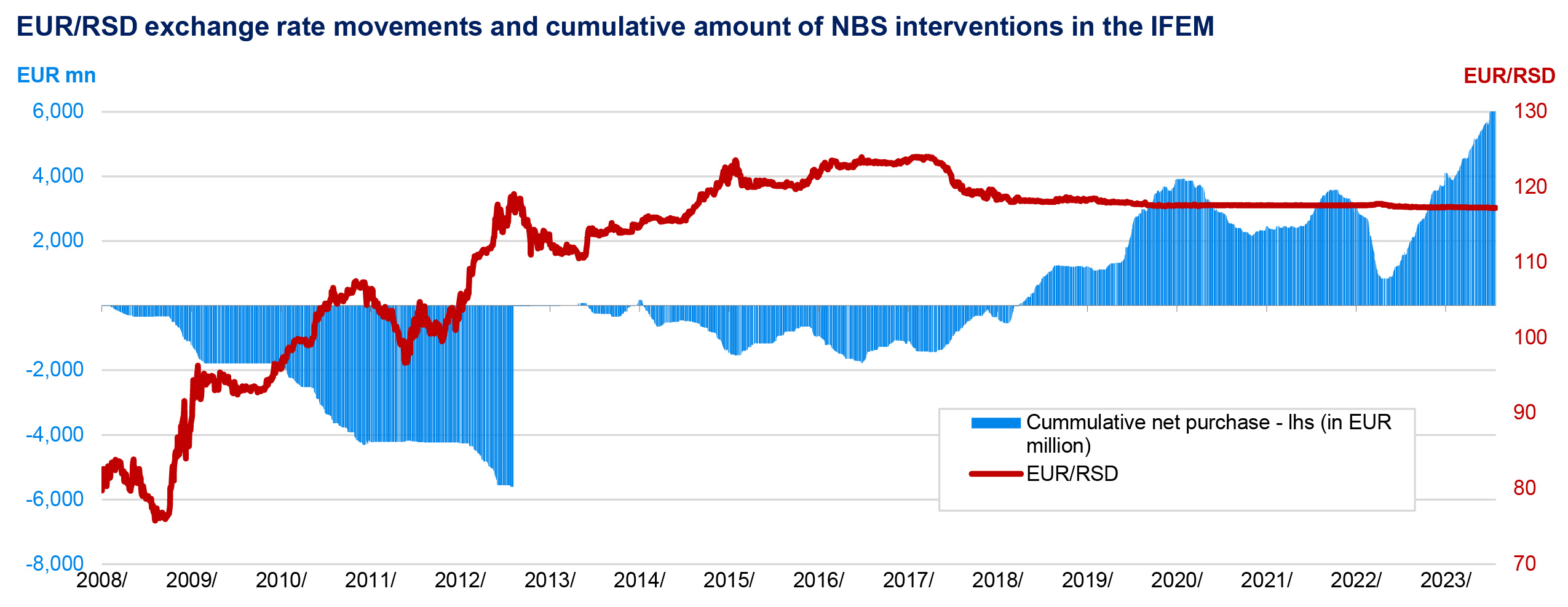

- The approach to the implementation of the RSD/EUR exchange rate policy was changed. Instead of tolerating significant volatility, which intensified inflationary pressures, business uncertainty, high exchange rate differences in the domestic economy and a rise in NPLs – all characteristics of the local market before August 2012, the NBS started to maintain relative exchange rate stability, by which it has been recognisable ever since.

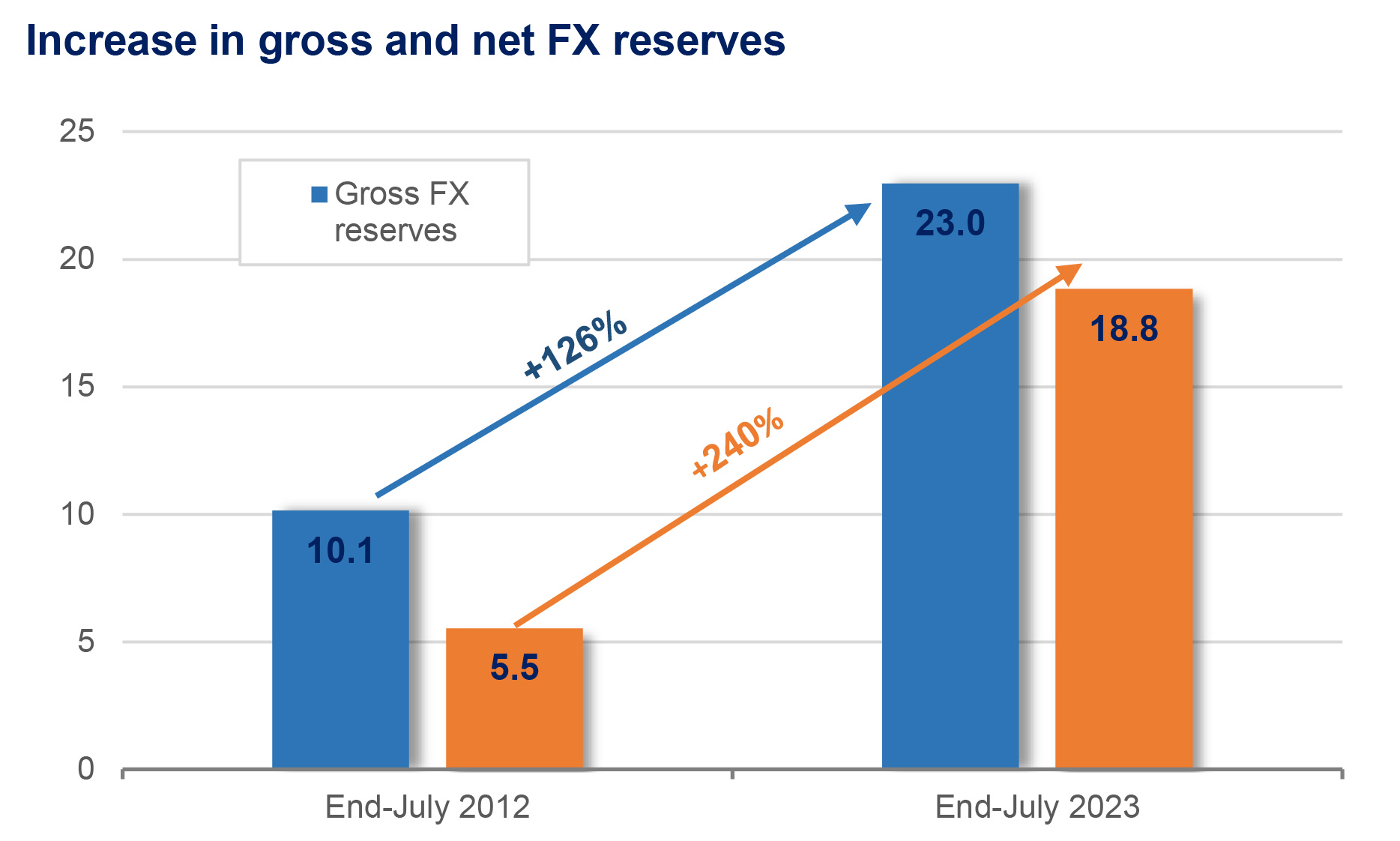

- The dinar strengthened against the euro in the last 11 years by 1.2% nominally. At the same time, the NBS always ensures that FX reserves are used prudently – in times of strengthened depreciation pressures, it invests in exchange rate stability, and in times of appreciation pressures, it increases FX reserves, building an additional buffer for the domestic financial system. Since 6 August 2012 until today, the NBS bought EUR 6.6 bn net in the IFEM and contributed, as the most significant individual factor, to more than doubling of the country’s FX reserves, which exceeded EUR 23 bn at end-July 2023, EUR 13 bn more (almost 130%) than at end-July 2012 (EUR 10.1 bn). Net FX reserves more than tripled in the same period (242% increase), rising from EUR 5.5 bn to EUR 18.9 bn.

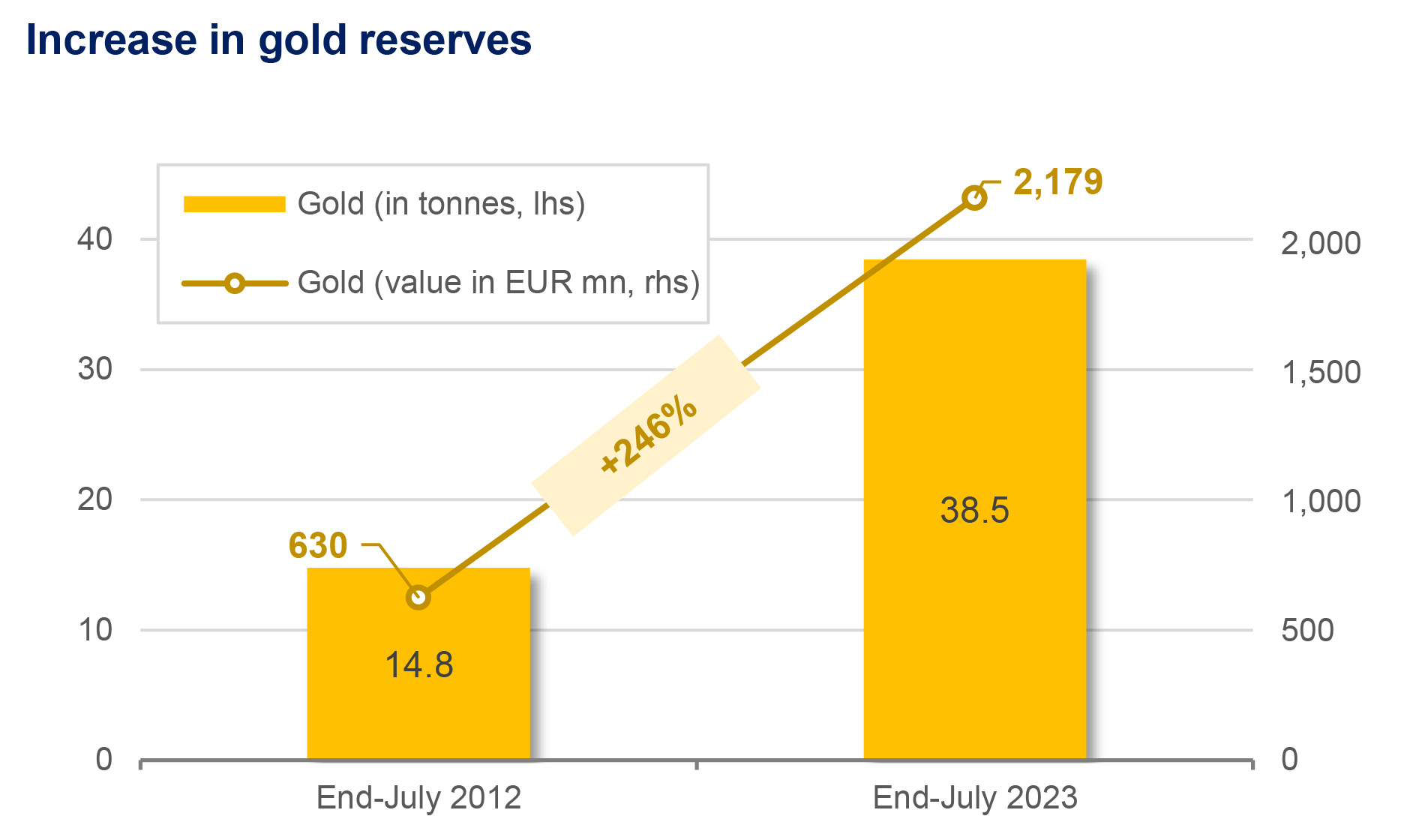

- The rise in FX reserves was accompanied by an improvement in their structure – we increased significantly the quantity, value and share of gold. Since August 2012, the quantity of gold has increased by over 2.5 times (from 14.8 tonnes at end-July 2012 to the current record 38.5 tonnes), with purchases in the international market (in 2019 and 2020, 12 tonnes in total), but also from domestic producers. It is noteworthy that the entire quantity of gold is of the highest quality and purity (over 99.5%). The share of gold in reserves rose from 6.2% to around 10%, and its value increased three and a half times (from EUR 0.6 bn to EUR 2.2 bn). As of July 2021, when we imported 13 tonnes of gold (1 tonne remaining from succession and 12 tonnes bought abroad), all gold reserves have been in Serbia, in the NBS vault.

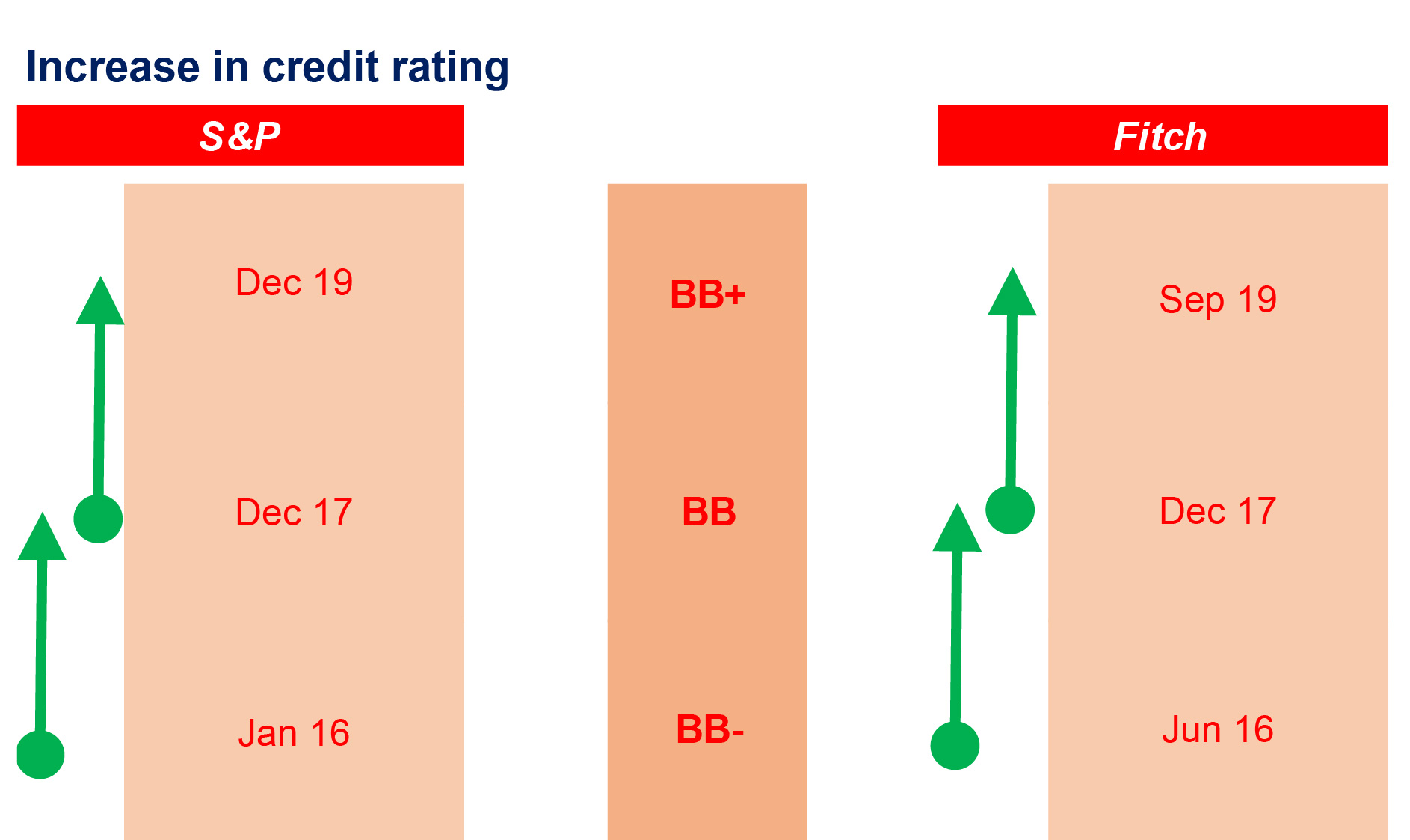

- Serbian credit rating went up by two notches, despite international crises, to a step away from investment grade.

- As a transformed country, Serbia has been recognised as an excellent investment destination. Investors state the following reasons, among other, for singling out Serbia as a good investment destination:

- relative stability of the exchange rate of the dinar against the euro;

- a track record of sound economic policies;

- commitment to the implementation of structural reforms and continuous improvement of business environment,

- uninterrupted investment cycle,

- high level of capital investment,

- strong and resilient banking sector;

- diversified export base that contributes to export sustainability even amid lower external demand.

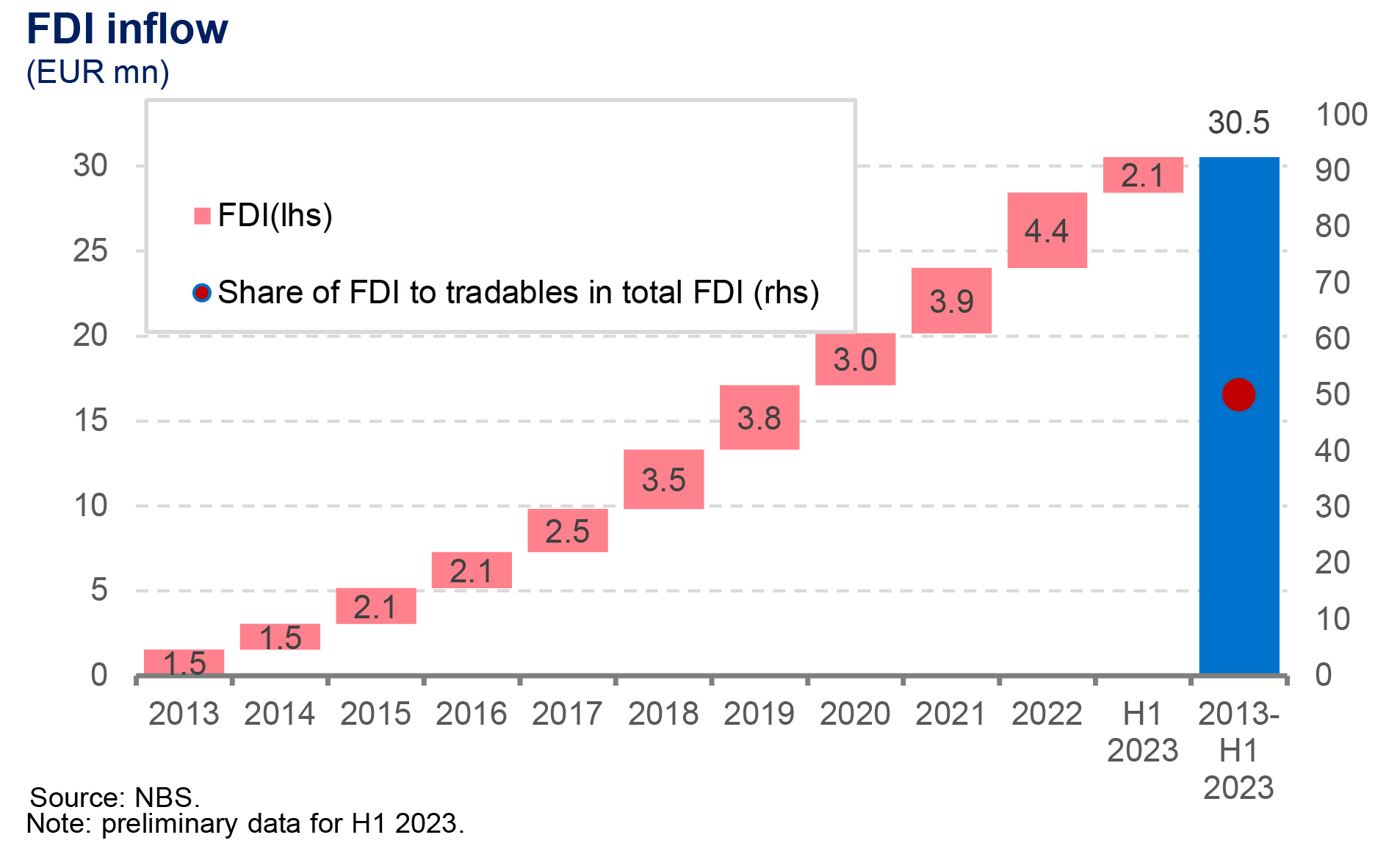

- Only in the last three and a half years marked by global shocks, EUR 13.5 bn of FDI was channelled to Serbia, оf which more than a half to tradable sectors. For our citizens this means new jobs, regular salaries, budget inflows, and, in turn, a stable and smooth functioning of the education system, health, security and everything else under government jurisdiction.

- Export of goods and services increased from EUR 11.5 bn in 2012 to EUR 38 bn in 2022, аnd this year we expect it to exceed EUR 42 bn.

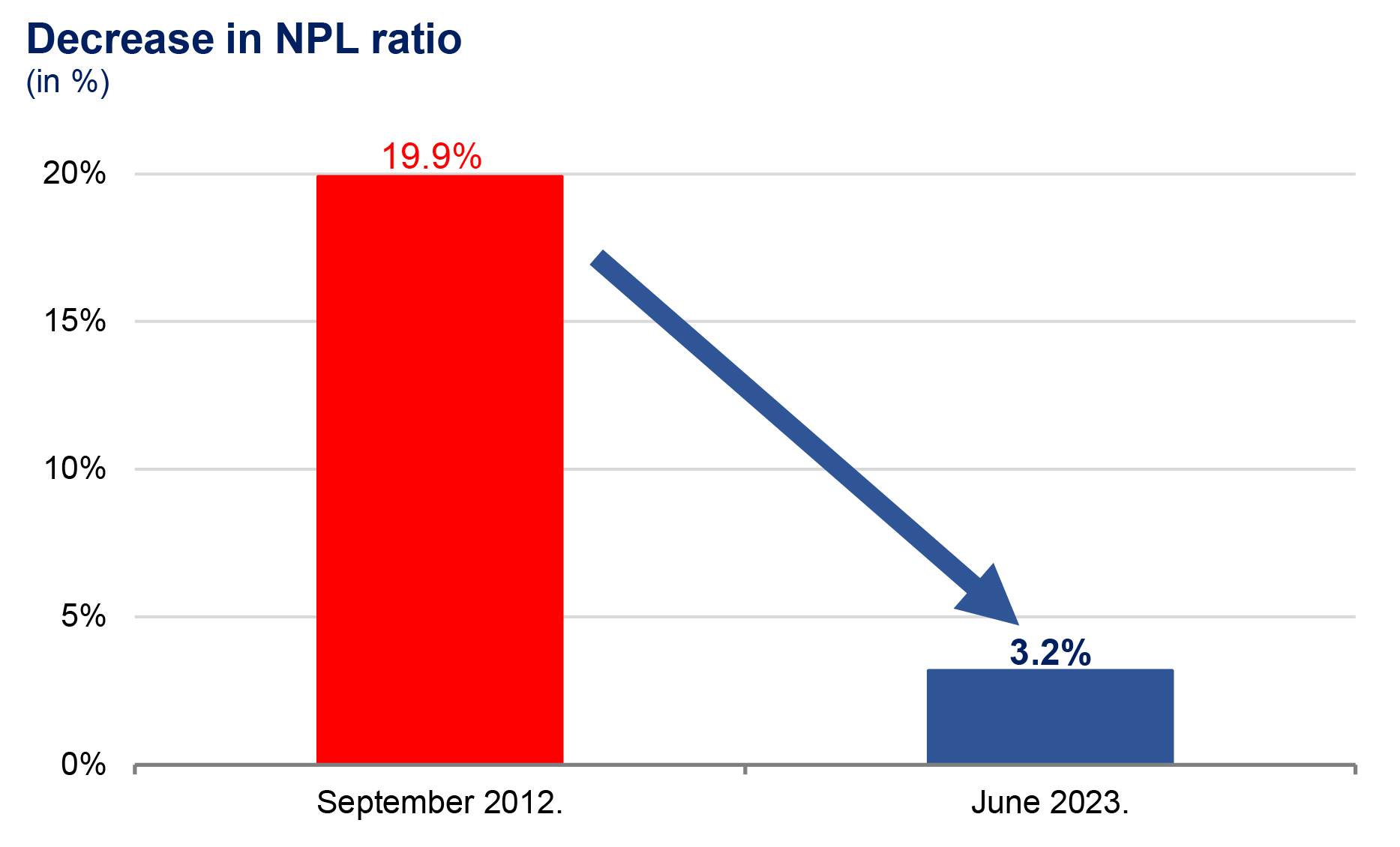

- The share of NPLs in total banking sector loans went down to around 3%, from around 20% in 2012 (a fifth of banking sector assets).

- The introduction of numerous new services as a competition to expensive foreign brands has helped boost the DinaCard turnover and halve the average merchant fee from 2.10% to 1.05%. Thanks to this alone, within the span of four years (2019–2022), savings of close to EUR 200 mn were made in the trade system, this being at the same time the cost that would have been passed onto buyers through the prices of goods and services.

The Banker, a reputable UK magazine owned by Financial Times, with almost a hundred years’ long tradition, proclaimed Jorgovanka Tabaković the best governor in the world and the best European governor for 2020. Among the reasons quoted were her contribution to the strengthening of the financial sector and stabilisation and growth of the Serbian economy.

We have steered the monetary system well through multiple challenges in the last three and a half years

Since December 2012, the NBS has conducted its main open market operations, reverse repo operations (repo sale of T-bills), used for withdrawing excess dinar liquidity on a weekly basis, under the multiple variable rate method. This method has provided the NBS with greater flexibility and efficiency in monetary policy implementation in the last 11 years. From the outbreak of the corona crisis, through energy and Ukraine crisis to globally elevated inflation, the NBS preserved stability in all segments of the domestic financial market. In previous years, we successfully used, but also innovated where there was a need, the existing monetary policy toolkit, using the familiar instruments from the global market (regular reverse and direct repo transactions, FX swap transactions, FX purchase and sale interventions, required reserve and remuneration rate, secondary purchase of government and corporate securities, etc.), responding adequately and timely to different types of challenges and thus increasing the efficiency of the achievement of the main NBS objectives.

Preserved and strengthened stability of the financial sector

In the last 11 years, with its actions the NBS ensured all the necessary preconditions for a sound and stable banking sector which finances the domestic economic activity and provides modern financial services.

- Due to operational problems caused by inappropriate management and supervision before 2012, we were forced to close four banks in the 2012–2014 period (Nova Agrobanka, Razvojna banka Vojvodine, Privredna banka Beograd and Univerzal banka Beograd). This laid the foundations for restoring confidence in the banking system, with all relevant indicators of banks’ performance significantly above NBS regulatory requirements.

- The NBS’s responsible approach was confirmed in 2022 in the resolution of the issue of Sberbank amid escalation of the Ukraine crisis in 2022, when the central bank’s fast and efficient response, which did not involve any spending of public funds, preserved the confidence in the Serbian banking sector.

- This confidence is unequivocally indicated by the rise in dinar and FX savings and their record levels (from below RSD 18 bn at end- 2012 to over RSD 110 bn, i.e. from EUR 8.3 bn to close to EUR 14 bn).

- Another proof of credibility of the NBS as a supervisor and regulator and the interest of foreign investors in the Serbian banking system are two greenfield investments from 2014 and 2016 (Mirabank and Bank of China Srbija), which contributed to the diversification of investments in the banking sector and improvement of economic cooperation with the home countries of those investors.

- Owing to the NBS’s responsible approach, consolidation of the banking system was implemented successfully, and stability was preserved even amid operational changes in some parent banks (e.g. during the Greek crisis in 2015). That the domestic banking market is attractive is evidenced by the fact that in this period the NBS granted 31 prior consents for acquiring bank ownership and 10 consents for mergers. The number of banks went down from 33 to 20, with continuous improvement of the quality and volume of services rendered to citizens and corporates.

- Faced with the pandemic and the negative effects of global shocks, we also enacted measures to facilitate loan repayment.

- In March 2020 - two days after the emergency situation in the country was declared, we adopted regulations introducing a 90-day moratorium on loan and financial leasing repayment for households and corporates, and in July 2020, an additional moratorium lasting from two to three months. Over 90% of debtors used the first moratorium and over 80% the second moratorium, which means that they were introduced for a reason and at the right moment. Banks’ deferred inflows on this account exceeded RSD 300 bn. These funds came to be additional disposable income that businesses and citizens could use for other priority needs and consumption.

- In December 2020, the NBS prescribed additional measures for rescheduling and refinancing the liabilities of the pandemic-affected debtors of banks and financial lessors. The facilities were used by over 50 thousand debtors, in the total amount of RSD 111 bn.

- In view of the economic situation in which some agricultural producers found themselves, and the strategic importance of agricultural production for citizens and businesses, in October 2022 the NBS enabled agricultural producers to reschedule their debt with banks and financial lessors. This measure provided for the rescheduling of 6,238 agricultural loans, including loans approved to persons engaging in the purchase and cold storage of fruit (RSD 24.2 bn, ending with June 2023).

- Support was given to citizens in financial distress by enabling banks to extend the repayment term of their cash, consumer and similar loans and thus help them in debt servicing and overcoming the challenges faced. We enacted measures facilitating the repayment of housing loans for citizens, whereby banks were further encouraged to extend the repayment term of these loans by additional five years relative to the initial maturity. As at end-June 2023, almost 2,000 debtors used the rescheduling of cash, consumer and similar loans and the extension of housing loan repayment term (RSD 2 bn in total).

- By supporting digitalisation of insurance services and improving the supervision of market conduct, the NBS contributed to the improved availability of and increased trust in insurance services. The NBS did this by insisting on better provision of information to clients, by preventing the spread of inadequate business practices and requiring prompt and efficient removal of any actions and activities that may have a potentially harmful effect on the rights and interests of insurance service users. The NBS supports innovation and the implementation of new technologies, while at the same time advancing the quality of insurance services.

- All relevant parameters in the insurance market displayed a positive trend in the past eleven years, with more than doubled capital, total assets, technical reserves, life and non-life insurance premiums, resulting in a generally positive trend of per capital premium and its share in GDP.

A large number of activities to protect financial service consumers

We implemented many activities within the new function of financial service consumer protection, which led to significant and direct positive financial effects for consumers:

- Based on the NBS Decision from 2015, banks returned to consumers around RSD 6 bn in respect of charging unilaterally changed interest rates.

- Based on an opinion issued by the NBS, from 2020/2021 banks return to consumers in the event of early loan repayment (reduce their outstanding debt) up to EUR 5 mn a year.

- Specific supervisory measures led to a write-off of consumers’ debt in the amount of around RSD 756 mn in the past three years.

- In the past three years, the direct positive effect for consumers whose complaints were founded came at around RSD 74 mn a year.

- We actively monitored banks’ market conduct. Due to unfair practices or acting contrary to regulations, we prohibited some banks from charging certain fees, thereby helping their clients save more than EUR 2.8 mn a year.

- We are one of the few countries that regulated in detail the advertising of financial services and brought this field into order, so now all data in the advertisements are accurate, unambiguous and complete.

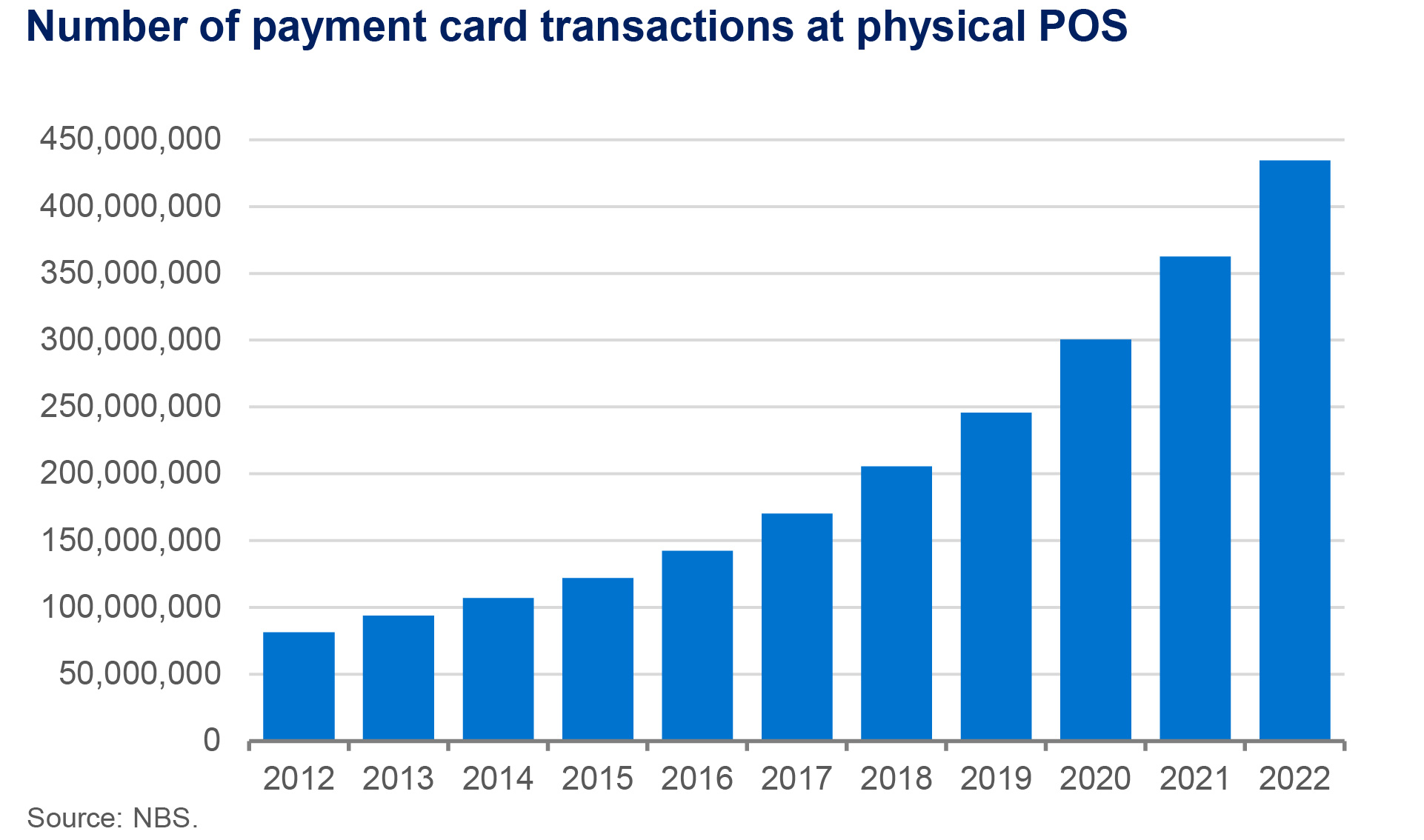

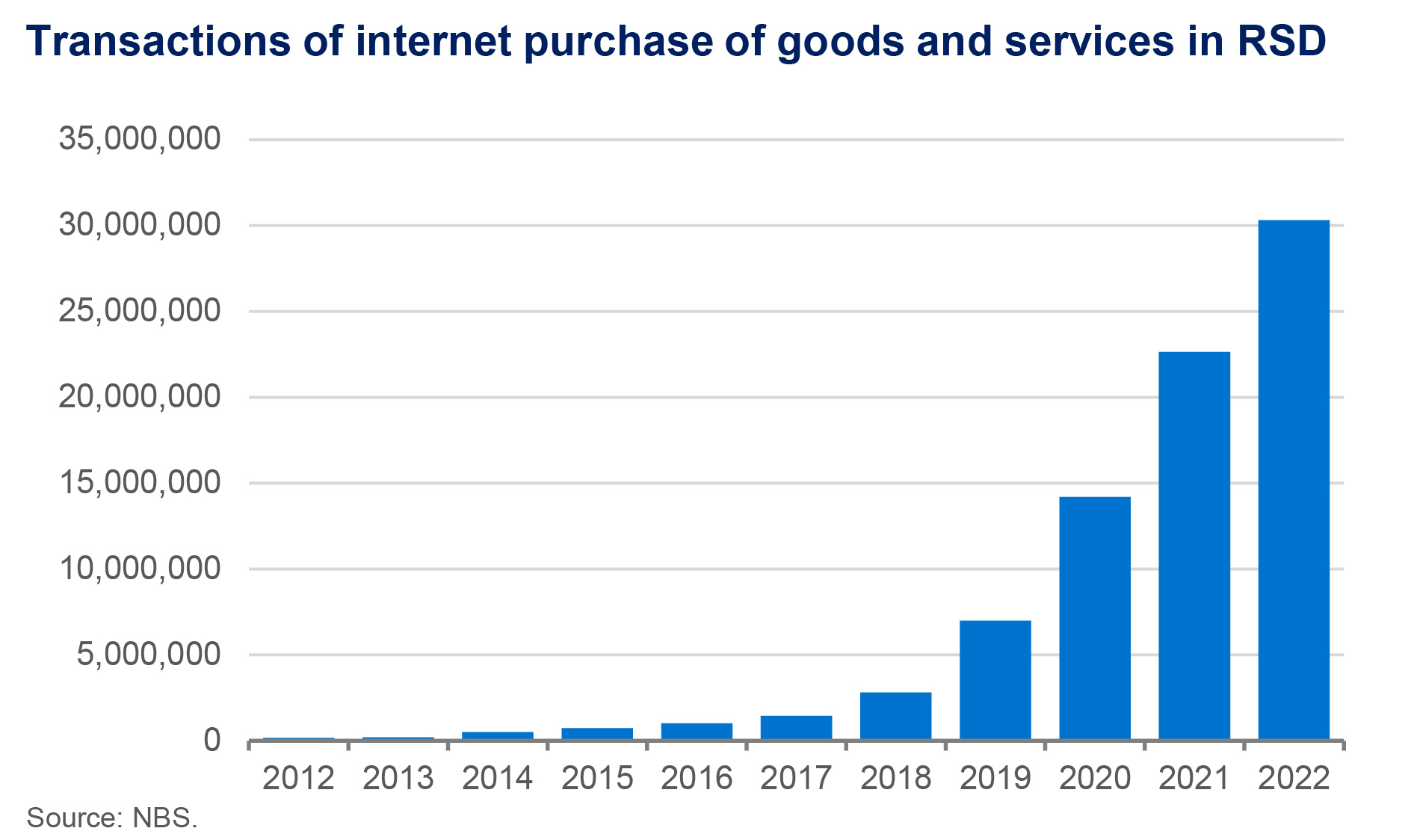

A safe card system and easier, cheaper, faster and innovative services

The NBS takes care of, monitors and promotes safe and stable functioning of six payment systems. Our activities have ensured operational reliability of all payment systems, as well as the security and efficiency of payment transaction execution in those systems.

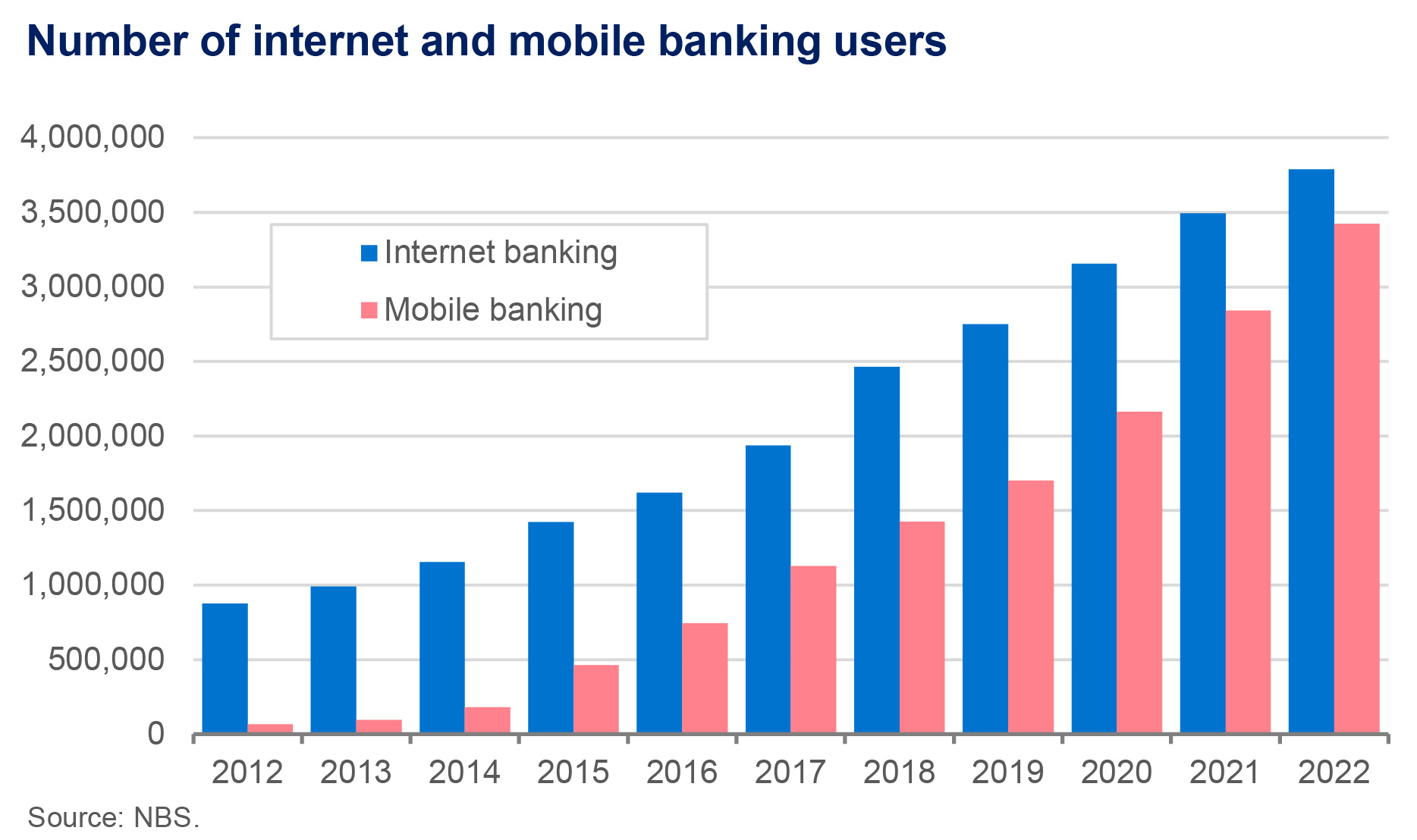

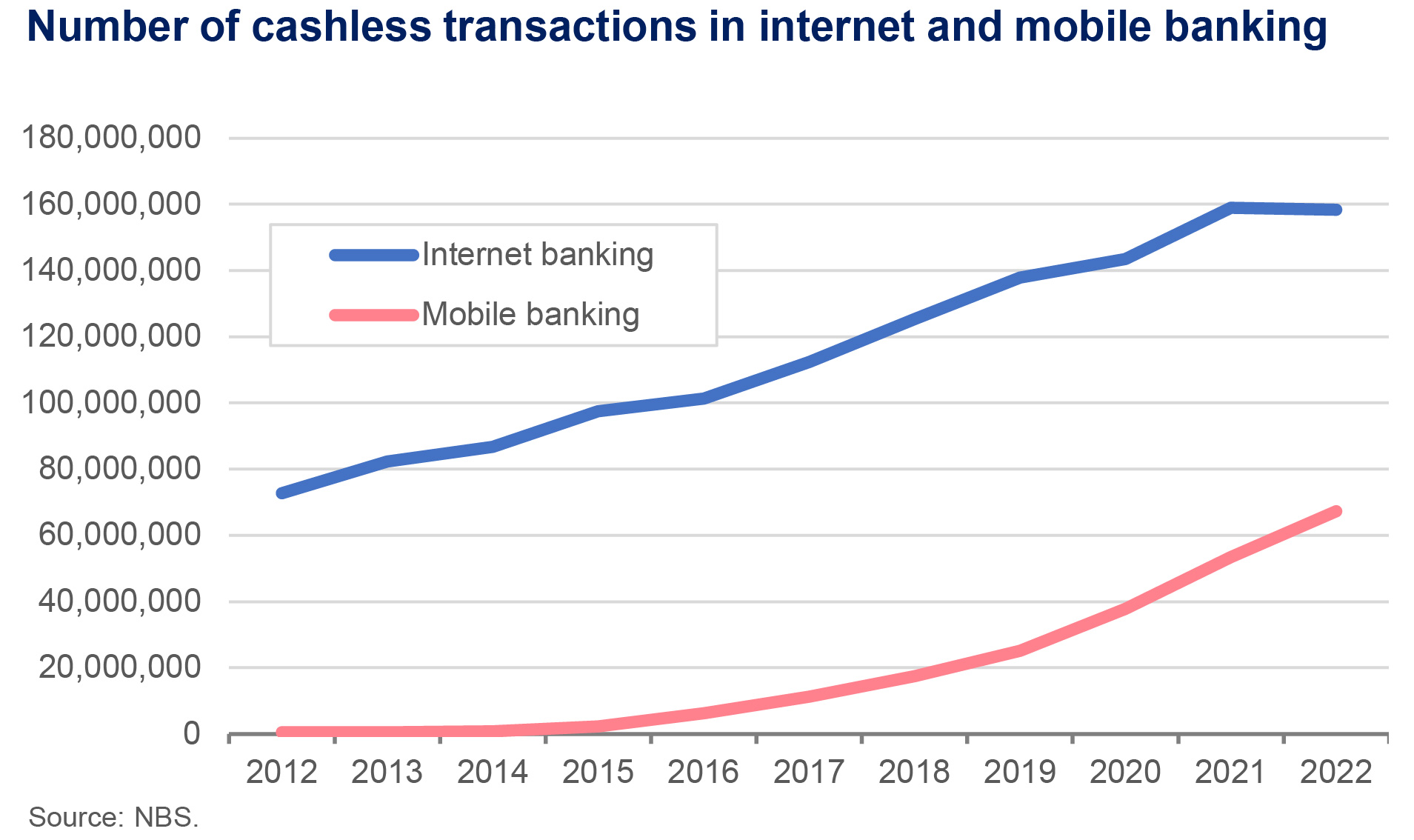

- The NBS-operated payment systems executed over 370 mn payments in 2022, almost double the number of payments in 2012.

- We introduced a modern legal framework for payment services, which promotes innovation and matches the best European and global practice. We were among the first in the world to have developed an instant payment system – the NBS IPS system, enabling citizens and businesses to make payments anytime and anywhere, with the money transferred to the payee’s account in no more than a few seconds.

- Citizens and businesses were given a remarkably simple model for paying their monthly utility and other bills by scanning the NBS IPS QR code (without typing in any data) via their m-banking apps.

- We enabled instant payments at POS using different methods (IPS show, IPS scan).

- Merchants were given a new, modern method of cashless payment at their POS, which ensures money disposal within a few seconds and at lower merchant fees, owing to the NBS’s price policy, as well as an independent development of solutions suited to their needs.

- Citizens were given an opportunity to execute instant payments in a simple way in their m-banking apps by entering only the mobile phone number of the payee registered for the service or by selecting the payee from the contact list, without the need to memorise any templates or to write down or enter the payee’s account number.

- With a view to implementing the projects of public administration digitalisation, we supported the E-Pay project, whereby Serbian citizens were enabled to pay for the services provided by the Ministry of the Interior in relation to the issuance of personal documents electronically, by simply scanning the NBS IPS QR code on the uniform payment slip generated on the E-Pay portal. In cooperation with banks, we provided for the possibility to execute all payments to “state” accounts as instant payments, thus eliminating the need for submitting any paper-based proof of payment.

- To buttress financial stability with regard to payment system independence, to cut down costs and modernise the domestic payment card, we worked strategically on the development of the DinaCard, our national card system.

- For instance, payment in instalments by the debit Dina card is indeed a great substitute for deferred payment by cheques. Given that this is a debit card, users can make deferred payments up to the amount of available account balances and they do not pay interest as in the case of credit cards.

- Cashback – in cooperation with banks and some merchants, we launched the cashback service, which implies that when making a purchase, Dina card users can withdraw free of charge cash up to RSD 5,000, this being particularly important for areas where ATM network is not as developed as in, for instance, big cities.

- The introduction of numerous new services as a competition to expensive foreign brands has helped boost the DinaCard turnover and halve the average merchant fee from 2.10% to 1.05%. Thanks to this alone, within the span of four years (2019–2022) savings of close to EUR 200 mn were made in the trade system, this being at the same time the cost that would have been passed onto buyers through the prices of goods and services.

- We upgraded the national card system – DinaCard also by introducing new technology (all new cards are chip-based) and card functionalities. The number of merchants enabling Dina card payments in their internet POS is increasing by the day (currently over 1,900 merchants). We have established successful cooperation with international card systems Union Pay and Discover, thus continuing to promote cross-border use of the national payment card.

- We adopted a set of measures that permanently protect the standard of citizens in terms of payment services that are needed for everyday life activities. The price of the payment account package with basic features was limited and prescribed to 150 dinars, its guaranteed content was specified, and an additional control mechanism of banks' actions was provided, in order to ensure future transparent and clear conduct.

Preservation of macroeconomic and financial stability and a favourable business environment through a gradual and selective liberalisation of capital flows

- Consistent with a gradual liberalisation of capital flows and acting in a preventative and measured way, the NBS managed in the current complex geopolitical circumstances to maintain stability, predictability and legality of capital flows and to ensure smooth cross-border payment transactions for household and corporate needs, all the while taking care of innovative forms of payment (e.g. enabling the collection of exports of IT sector services through PayPal from 2015 or giving Serbian residents the possibility to sell applications on the Play Store).

- The NBS took over from the Ministry of Finance – Tax Administration the supervision of exchange and foreign exchange operations as of 1 January 2019, thereby rounding off its regulatory and supervisory role in these areas.

Significant savings in terms of exchange rate application

- The security and protection of the citizens of the Republic of Serbia in the exchange market have been improved and the safe and smooth performance of exchange operations has been ensured even in the conditions of the pandemic.

- The long-standing issue of charging for travel arrangements according to banks’ selling rates for foreign exhange or foreign cash has also been resolved. From the end of July 2019, when stating the price and charging for travel arrangements abroad, the official middle exchange rate of the dinar is applied.

- The lowest buying rate and/or the highest selling rate that authorised exchange dealers and the public postal operator can apply when buying or selling foreign cash - euros, is limited to ±1.25% in relation to the official middle exchange rate of the dinar against the euro, which is valid on that day, and the exchange commission is capped at 1%.

Modern, reform laws and regulatory arrangements benefiting citizens and corporates

Owing to its proactive and advanced approach, the NBS has been recognised as the frontrunner in initiating and implementing modern regulatory arrangements in the financial sector adjusted to the needs of citizens and businesses.

The prominent role of the NBS in the domain of regulatory activities manifested through legislative initiatives and prepared proposals of laws adopted by the National Assembly, as well as through the adoption of numerous by-laws and participation in other regulatory reforms which improved the business environment in the country, facilitated lending, modernised payment services and strengthened the protection of financial service consumers in all segments.

Our numerous regulatory activities enabled:

- establishment of a modern legal framework during the Governor’s first office, which provides the NBS with adequate tools for implementing monetary and exchange rate policies and reinforcing the independence and autonomy of the NBS, as the central bank, precisely for that purpose (amendments and supplements to the Law on the National Bank of Serbia from 2012, 2015, and 2018);

- change of the bank resolution framework which ensures continuity of the bank’s critical functions, full protection of depositors and minimum cost for the government (amendments and supplements to the Law on Banks from 2015), which proved effective in practice in case of Sberbank;

- creation of an ecosystem for innovative solutions in the digital assets market and its proper development (the Law on Digital Assets and all by-laws for the implementation of that law), with the appearance of the first entities licensed by the NBS to operate with virtual currencies in the domestic market in accordance with international standards;

- modernisation in the provision of payment services in the country and abroad and greater competition in the payment services market (the Law on Payment Services);

- harmonisation and lowering of payment transaction costs and their greater transparency for citizens and businesses (the Law on Multilateral Interchange Fees and Special Operating Rules for Card-based Transactions, Decision on the Payment Account with Basic Features);

- greater protection and improved position of financial service consumers (amendments and supplements to the Law on the Protection of Financial Service Consumers), especially in conditions of increasing use of information-communication technologies (the Law on the Protection of Financial Service Consumers in Distance Contracts);

- introduction of financial collateral in line with international standards in the domestic financial market, aimed at improving legal security and efficiency in fulfilling obligations in the financial market, reducing credit and systemic risks (the Law on Financial Collateral) and contributing to the development of the financial market;

- improvement of the legal framework governing the capital market, through active participation in the drafting of the new Law on the Capital Market, as well as strategies for the development of the capital market;

- activities aimed at improving and expanding the use of cashless payments in the context of programmes and strategies to combat the grey economy, in cooperation with the government and relevant ministries.

Significant legislative activities of the NBS, carried out in cooperation with other competent authorities, have improved the AML/CFT legal framework, while honouring the use of modern technological tools in the financial sector (e.g. we were among the first in Europe to regulate video-identification of clients, with a number of users identified in this way increasing year by year – the Decision on Conditions and Manner of Establishing and Verifying Identity of a Natural Person through Means of Electronic Communication). The significant role of the NBS in this area was recognised by relevant international institutions (FATF and MONEYVAL), which assessed with the highest grades not only the compliance with international standards of regulations governing the operations of financial institutions supervised by the NBS, but also the efficiency of their implementation.

The Institute for Manufacturing Banknotes and Coins (ZIN) has regained its status as the leading security printing institution in the region

- As a specialised part of the NBS, by making use of decades-long experience, modern technology, and the specific work organisation, ZIN has expanded its range of products and restored the status of the leading security printing institution in the region in the past 11 years.

- In addition to regularly supplying the NBS with banknotes and coins, ZIN provides all the state bodies and citizens with security products of the highest level.

- ZIN produces passports, ID cards, driving and vehicle licences, vehicle registration plates, health insurance cards, excise tax stamps for coffee, tobacco and alcohol, weapon registration cards and permits to carry a weapon, hunting and recreational fishing permits, tourist vouchers, visas for foreigners, birth certificates, tax stamps, control labels for marking medications, passports for pets and cattle, motor liability insurance policies, tachograph cards for truck transport, certificates for professional drivers, all banking sector cards (Dina, Visa, Master), as well as many other products citizens need daily.

- The tradition of printing banknotes for the foreign market continued. In addition to card products, as the most modern among highly protected products, the range of minted products has been upgraded. What stands out in particular is the project of making silver coins with the image of Nikola Tesla, which are commissioned for the markets of the USA, Hong Kong, and China.

- Business results recorded by ZIN in recent years are record-breaking in the last three decades. Successfully organised production processes, as well as equipment modernisation, contributed to ZIN’s historical progress.

- Intensive activities in recent years resulted in ZIN’s operating according to the strictest rules of the industry, applying the requirements of the most complex ISO standards, thus guaranteeing not only the quality, but also the safety of its products. In addition, amid increasing global pollution, ZIN decided to conduct its business activities in accordance with the principles of environmental protection and social responsibility.

The NBS contributes significantly to Serbia’s credibility in the international community

Many international institutions point out that Serbia has proven to be a country capable of responding successfully to various shocks from the international environment over an extended period:

- In its latest report from June 2023, the IMF assessed that in the last decade, despite external shocks, Serbia achieved impressive economic results, reflecting its strong economic policy. Such a policy supported robust growth, low inflation, and a reduction in public debt, leading to increased income and employment, and improved standard of living. FX reserves are significantly higher, and FDI inflow reached record levels.

- All investors agree that Serbia’s macroeconomic fundamentals are excellent, and that Serbia has long deserved an investment-grade rating. Serbia is a country which has accomplished much in recent years, and has proven its ability to maintain stability and remain on growth trajectory in all conditions, thanks to credible policies. The manner and speed of response to numerous shocks preserved the necessary confidence in policymakers, as a guarantee of stability in all circumstances. Investors emphasise credible monetary policy, sound fiscal policy, high FX reserves, strong and diversified FDI, characteristic for Serbia for a decade now.

- Serbia’s upgraded credit rating, a notch from investment grade, despite pronounced global uncertainty, also speaks about the positive perception of Serbia as an investment destination. In their assessments, rating agencies particularly emphasise the proven credibility of monetary policy and overall economic policy, the significance of high FX reserves, and the relatively stable exchange rate of the dinar against the euro, favourable long-term growth prospects for Serbia, fiscal discipline, and the declining public debt trajectory.

NBS and the European integration process – all chapters led by the central bank opened

- In the European integration process, we take a significant part in the work of 8 negotiating groups. We have a leading role in the most important economic chapters – Financial services and Economic and monetary policy, chaired by the NBS, Free movement of capital co-chaired by the NBS.

- All three chapters are open.

Investing in human capital, because people are the pillar of institutions and the engine of progress

- We have signed 16 memoranda of business cooperation with higher education institutions in the Republic of Serbia, as well as six memoranda with faculties from the Republic of Srpska.

- Over the past eleven years, more than 700 students had the opportunity to acquire professional knowledge and many even started a professional career through student internship programmes.

- The lasting success and undeniable results accomplished by the NBS in the past 11 years were achieved by applying a simple principle – employees, their expertise and professional competencies are the most important capital of an institution.

“Even in times of global uncertainty, Serbia proved a country able to successfully preserve stability, thanks to firm and timely decisions and measures taken by Serbian leaders headed by President Aleksandar Vučić. We proved that it is possible to act in the general interest even when there are great expectations from the regulator and inherited excessive freedoms in the name of the market. I am thankful to those who understood that everything we do, we do with people and for people. Monetary and financial stability has been and remains our vision and strategy. They bring welfare to everyone and enable growth and development of our country as well as better living standards. We will justify their trust with our results in the period ahead. I believe and know that politics must serve the economy and people. If that is not the case, it will not stand the reality check. And reality is changing. There will be seemingly new theories brought by globalisation and technological development, but the fundamental postulate will remain unchanged – stability has no alternative. Only in this way can we preserve and protect Serbia,” concludes Governor Jorgovanka Tabaković.

Видео:

Governor's Office